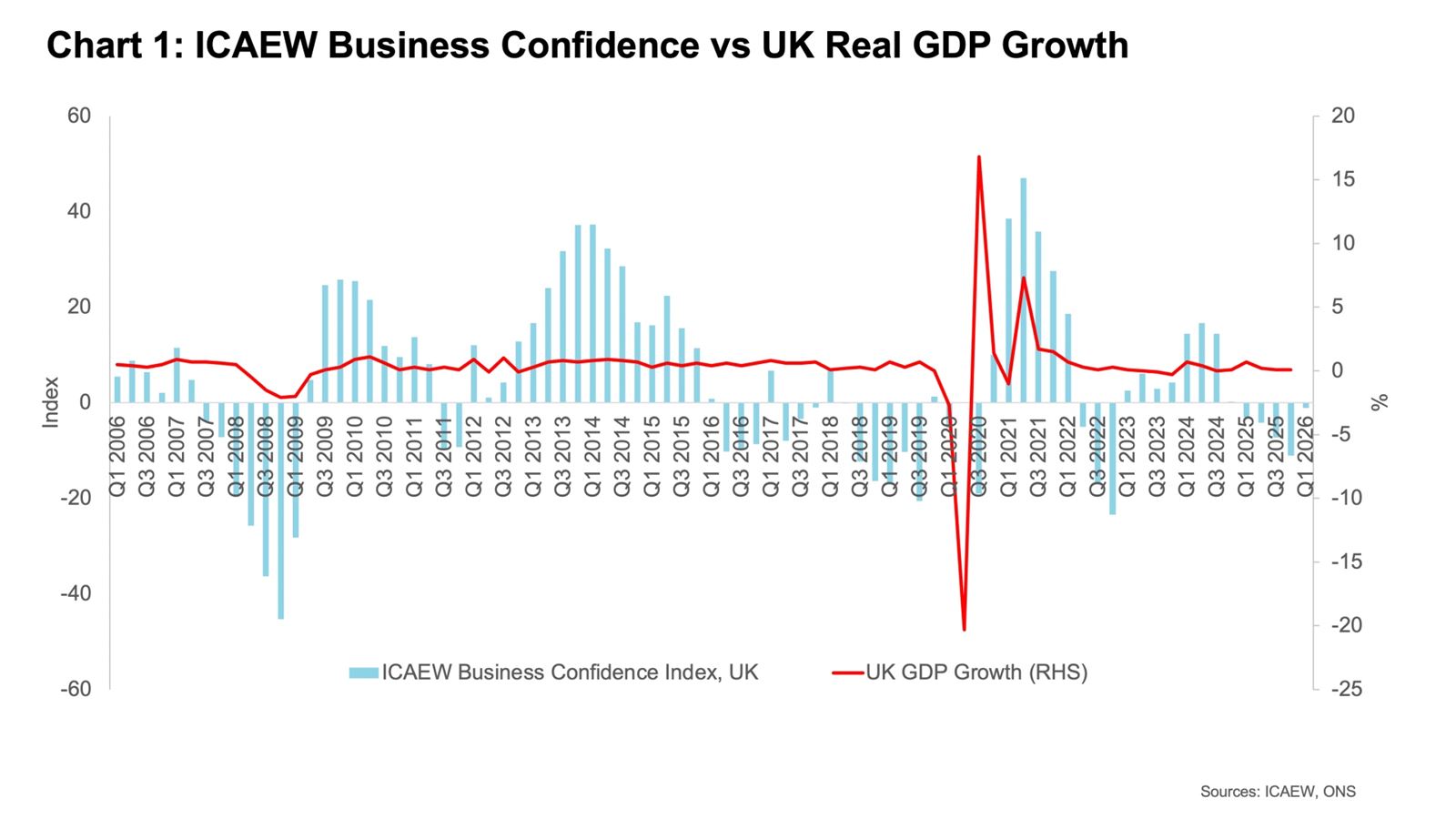

UK Business Financial Distress Surges 37% as Cost Pressures Bite Across All Sectors

The number of UK businesses in critical financial distress has surged by nearly 37% in the first three months of 2026 compared to the same period last year, according to research from BTG Consulting. The data, drawn from the Red Flag Alert monitoring system, paints a stark picture of an economy under severe strain, with 62,193 companies now classified as critically distressed — up from 45,416 in Q1 2025. Every single one of the 22 industries tracked has seen double-digit percentage increases.Background

The UK economy entered 2026 in a fragile state, battered by the combined effects of elevated interest rates, persistent inflation, rising employer costs, and the economic disruption caused by the ongoing conflict in the Middle East. The Bank of England held interest rates at 3.75% in April 2026 but signalled the possibility of further increases if inflation — which ticked up to 3.3% in March — continues to rise. Brent crude oil has been trading at around $111 per barrel, driven by tensions around the Strait of Hormuz, adding to energy costs for businesses across the country.

The increase in employer National Insurance contributions, which came into effect in April 2025, has added significantly to the cost base of businesses across all sectors. Combined with rises in the national minimum and living wages, many employers — particularly in labour-intensive sectors such as hospitality, retail, and social care — have found their margins squeezed to breaking point. The Red Flag Alert system, which monitors financial indicators across UK companies, has been tracking a deteriorating picture since the second half of 2025.

The backdrop of geopolitical uncertainty has compounded domestic pressures. The Iran conflict has disrupted global supply chains and pushed up energy and materials costs, while the threat of further US tariffs on UK exports has created additional uncertainty for manufacturers and exporters. Business confidence, as measured by the Institute of Directors, remains deeply negative, with many firms planning hiring freezes or redundancies.

Key Developments

BTG Consulting's research shows that critical financial distress — defined as companies showing the most severe indicators of financial difficulty, including county court judgements, winding-up petitions, and significant deterioration in financial ratios — rose to 62,193 in Q1 2026. The sectors with the sharpest increases include Hotels and Accommodation (+69.3%), Leisure and Cultural Activities (+65.9%), and Sports and Health Clubs (+51%). These are precisely the sectors that were hardest hit by the pandemic and have never fully recovered their pre-2020 financial resilience.

The number of companies in "significant" financial distress — a less severe but still serious measure — also rose by 9.6% annually to 634,867. This broader figure suggests that the pipeline of companies moving towards critical distress is substantial, and that the headline figure of 62,193 is likely to grow further in Q2 2026 unless economic conditions improve markedly.

The research also highlights the impact of the UK's high tax burden on business viability. Corporation tax remains at 25% for larger companies, and the combination of employment taxes, business rates, and VAT creates a cost environment that many smaller businesses describe as unsustainable.

Why It Matters

Business distress at this scale has consequences that extend well beyond the companies themselves. When businesses fail, jobs are lost, supply chains are disrupted, and communities lose services and economic activity. The concentration of distress in hospitality, leisure, and retail — sectors that are central to the economic life of town centres across the UK — means that the visible impact on high streets and local economies will be significant.

This is the third consecutive quarter in which critical distress has risen sharply, suggesting this is not a temporary blip but a structural deterioration. For context, the previous peak in business distress was during the pandemic in 2020-21, when government support schemes — furlough, bounce-back loans, and business rates relief — provided a significant buffer. No equivalent support is currently available, and the government has signalled that fiscal constraints make large-scale intervention unlikely. Unlike Ireland, where the government has maintained a more active industrial policy and where corporate tax revenues from multinationals provide a significant fiscal cushion, the UK government has limited room for manoeuvre.

Local Impact

The impact of rising business distress is being felt across every region of the UK. In Northern Ireland, where the economy is particularly dependent on small and medium-sized enterprises in retail, hospitality, and construction, the figures are especially concerning. Belfast city centre has seen a number of high-profile closures in recent months, and the hospitality sector — which had been recovering strongly after the pandemic — is once again under severe pressure. In Scotland and Wales, where devolved governments have some ability to provide business support, there have been calls for emergency measures to prevent a wave of insolvencies in the coming months.

What's Next

The Insolvency Service is expected to publish its Q1 2026 corporate insolvency statistics in the coming weeks, which will provide a further measure of the scale of business failures. The Bank of England's Monetary Policy Committee meets again in June, and its decision on interest rates will be closely watched by businesses struggling with debt servicing costs. The government's forthcoming spending review, expected in the autumn, will determine whether any additional support for distressed businesses is available. Business groups including the CBI and the Federation of Small Businesses are calling for an emergency review of employer National Insurance contributions.

Sources: Investing.com / BTG Consulting | Credit Protection Association