UK Mortgage Affordability at Worst Level Since 2008 as Inflation Climbs to 3.3% on Energy Shock

British households are facing a double economic squeeze not seen since the aftermath of the 2008 financial crisis, with inflation rising to 3.3% on the back of soaring energy costs driven by the Middle East conflict, and mortgage affordability reaching its most constrained level in nearly two decades — a combination that is eroding living standards across the UK and forcing the Bank of England into an increasingly difficult balancing act.Background

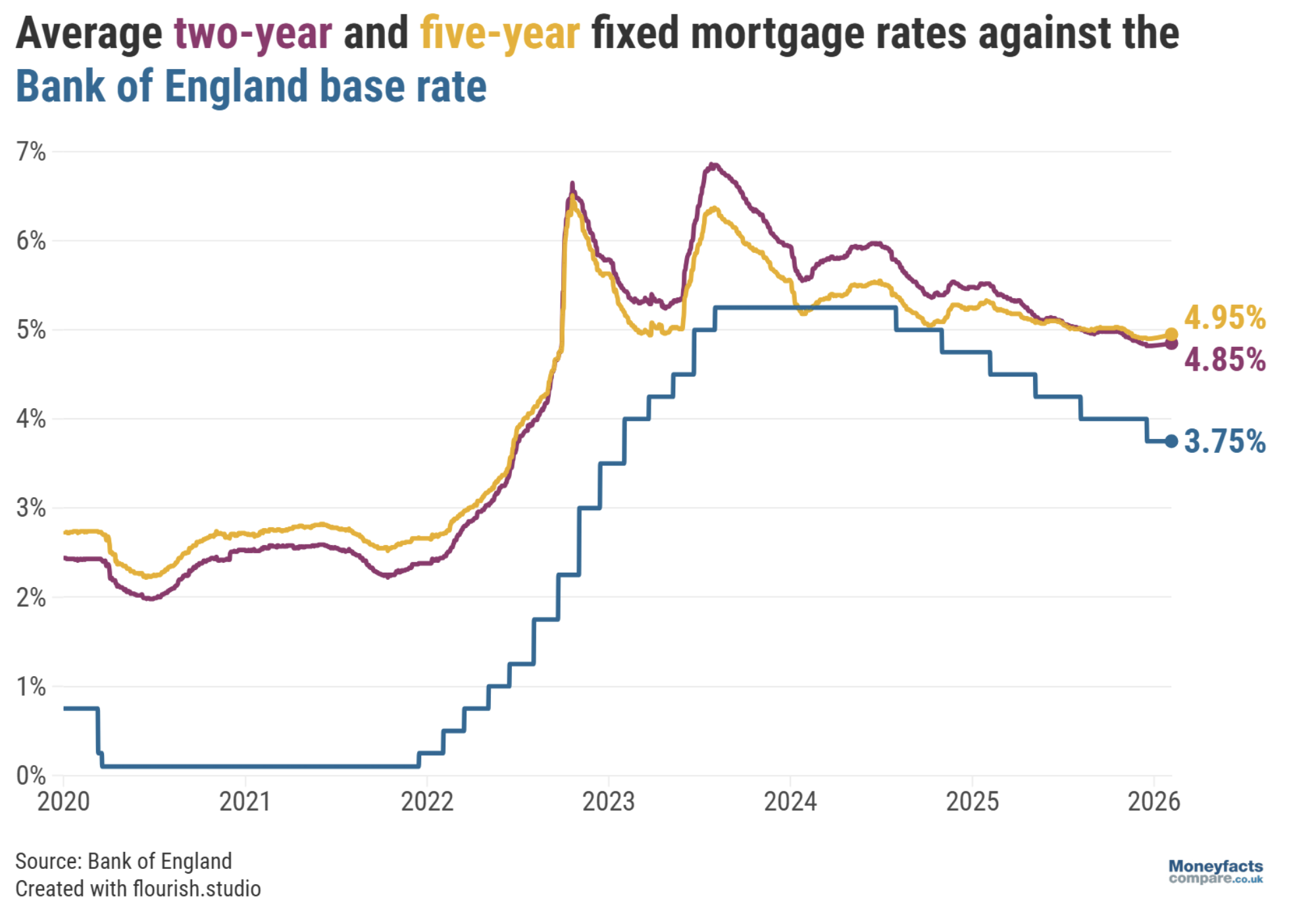

The UK economy entered 2026 in a fragile state, having navigated the post-pandemic recovery, the 2022 energy crisis, and the inflationary surge that followed Russia's invasion of Ukraine. The Bank of England had been cautiously cutting interest rates through 2025, bringing the base rate down from its peak of 5.25% to 3.75% by early 2026, providing some relief to mortgage holders and businesses. That trajectory has now been thrown into reverse by the outbreak of the Middle East conflict, which has disrupted global oil and gas markets and sent energy prices surging once again.

The UK is particularly exposed to global energy price shocks because of its relatively limited domestic production capacity and its dependence on imported liquefied natural gas. The conflict has also disrupted shipping routes through the Strait of Hormuz, adding further pressure to global commodity markets. Brent crude briefly exceeded $125 per barrel in the weeks following the conflict's escalation — a level not seen since the immediate aftermath of Russia's invasion of Ukraine in 2022.

The housing market, meanwhile, has been in a state of fragile equilibrium. House prices have remained elevated relative to incomes, supported by constrained supply and persistent demand, but the affordability of mortgages has been deteriorating as fixed-rate deals taken out during the ultra-low interest rate era of 2020-2022 have expired and been replaced at much higher rates.

Key Developments

The UK's Consumer Price Index rose to 3.3% in March 2026, up from 3.0% in February, according to data published by the Office for National Statistics. The primary drivers were transport costs — motor fuel prices have climbed 20% since the conflict began — and a sharp rise in airfares. Food price inflation, which had been easing, has also ticked upward as supply chain disruptions feed through to supermarket shelves.

The Bank of England's Monetary Policy Committee voted 8-1 to hold the base rate at 3.75% at its April meeting, with one member voting for an increase to 4%. Governor Andrew Bailey stated that the future direction of rates depends on the "size and duration of the shock to energy prices," and the Bank has outlined three scenarios: in the worst case, if oil prices rise above $130 per barrel and remain elevated, inflation could peak at over 6% by early 2027 and rates may need to rise to 5.25%.

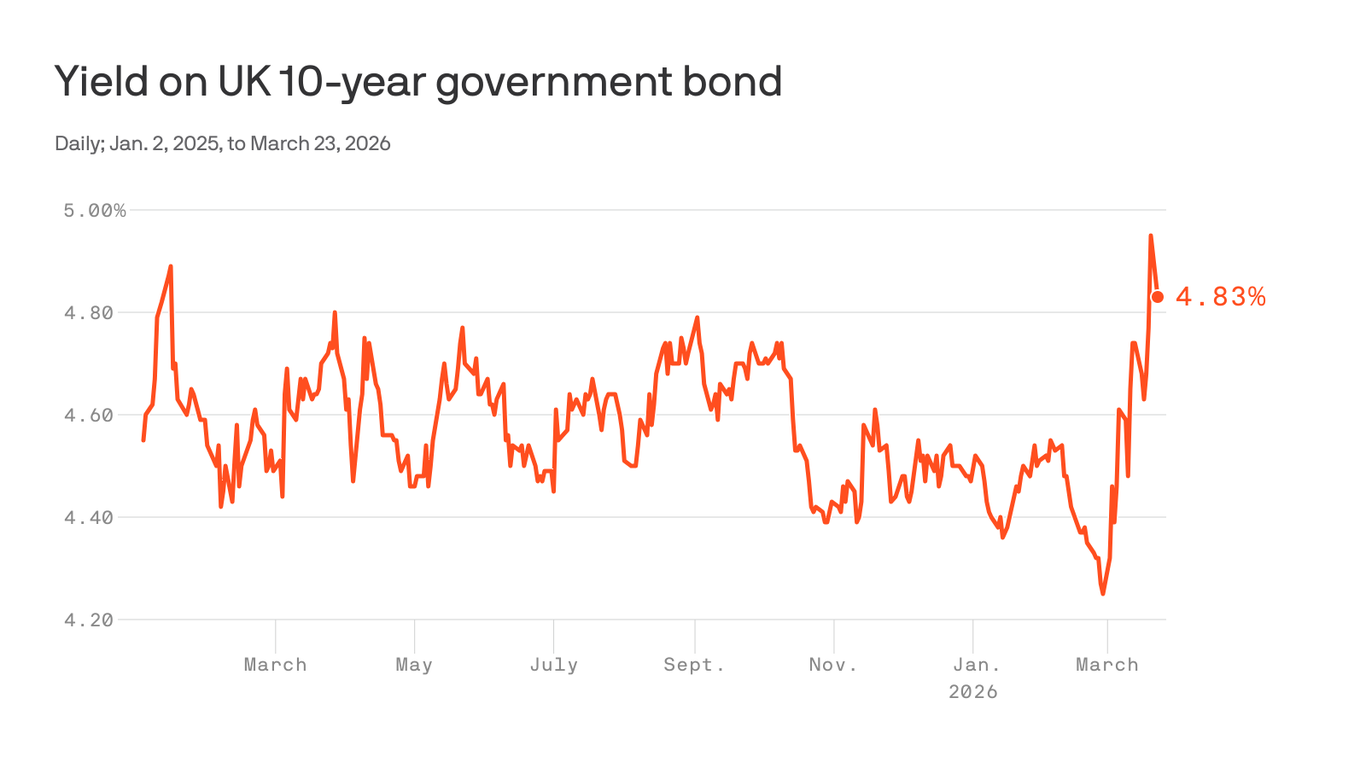

On mortgages, the picture is stark. The average rate on a new two-year fixed mortgage reached 5.79% by the end of April 2026, up from 4.83% in March — a rise of nearly a full percentage point in a single month. An estimated 800,000 fixed-rate mortgages with rates of 3% or less are due to expire annually through the end of 2027, forcing homeowners to remortgage at dramatically higher rates. UK Finance has described affordability as being at its tightest level since 2008.

Why It Matters

The convergence of rising inflation and deteriorating mortgage affordability is not merely an economic statistic — it represents a genuine crisis of living standards for millions of British households. A family remortgaging a £250,000 home from a 2% fixed rate to a 5.79% rate faces an increase in monthly payments of approximately £600 — a sum that, for many households, represents the difference between financial stability and genuine hardship. This is the third major cost-of-living shock in four years, following the pandemic and the 2022 energy crisis, and there is a real risk that the cumulative effect is more damaging than any individual episode.

For context, the UK's mortgage market is more exposed to interest rate changes than many of its European peers, because a higher proportion of UK mortgages are on short-term fixed rates rather than the long-term fixed rates common in Germany and France. This means that Bank of England rate decisions feed through to household budgets more quickly and more painfully in the UK than elsewhere. The next MPC meeting is scheduled for June 18, and markets are pricing in a significant probability of a rate increase — which would add further pressure to an already strained housing market.

Local Impact

In Northern Ireland, the mortgage affordability crisis is compounded by the region's unique energy vulnerability. Households facing higher mortgage payments are simultaneously dealing with home heating oil costs that have more than doubled since the start of the conflict. In Belfast, where house prices have risen significantly over the past decade, first-time buyers are finding the market increasingly inaccessible. In the Republic of Ireland, the Central Bank has maintained its mortgage lending rules, which have provided some protection against the worst excesses of the housing market, but Irish households are equally exposed to the energy price shock and the broader inflationary environment.

What's Next

The Bank of England's next rate decision is on 18 June 2026. The Office for National Statistics will publish April inflation data in mid-May, which will be the first reading to fully capture the impact of the conflict on consumer prices. Readers should watch for: any emergency fiscal measures from the Treasury to support mortgage holders; the Bank of England's May Monetary Policy Report, which will include updated economic forecasts; and whether the government's planned mortgage guarantee scheme is extended or expanded in response to the affordability crisis.

Sources: UK Finance — Monthly Economic Review May 2026; BBC News — UK interest rates and mortgages