UK Borrowing Costs Hit Highest Level Since 1998 as Iran Conflict Rattles Markets

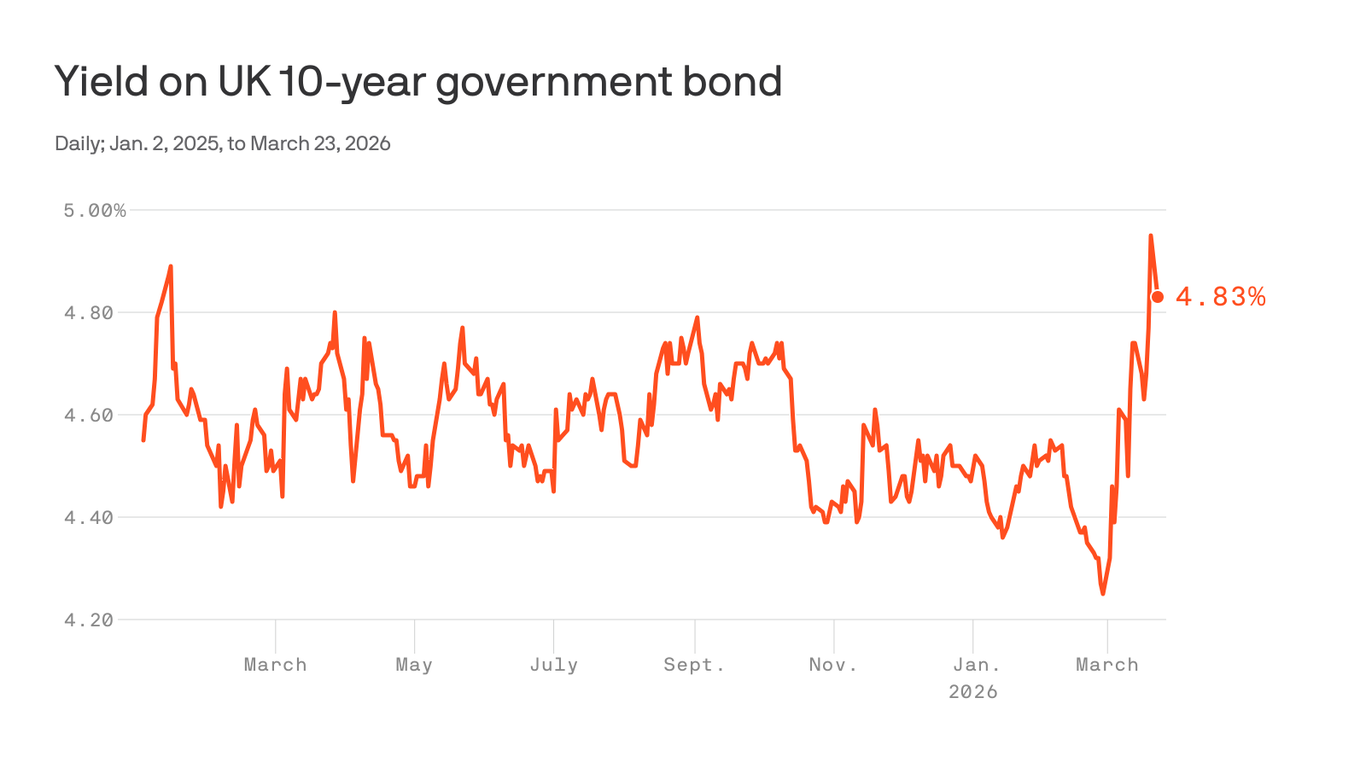

British government borrowing costs have surged to their highest level since 1998, with thirty-year gilt yields climbing to 5.78% and ten-year yields breaching 5%, as the ongoing US-Iran conflict, rising oil prices, and political uncertainty ahead of Thursday's local elections combine to unsettle financial markets.

Background

Gilt yields — the interest rate the UK government pays to borrow money — are a fundamental indicator of the country's fiscal health and the confidence of international investors in British economic management. When yields rise, borrowing becomes more expensive for the government, which in turn constrains public spending, increases pressure on the deficit, and can feed through into higher mortgage rates and business loan costs for ordinary households and companies.

The last time UK borrowing costs were at these levels was in 1998, during a period of global financial turbulence following the Asian financial crisis and the Russian debt default. The comparison is instructive: then, as now, the spike was driven by external shocks rather than domestic policy failures — but the political consequences were nonetheless severe. The current government inherited a difficult fiscal position from its predecessor, and the additional pressure from rising gilt yields narrows the Chancellor's room for manoeuvre considerably.

The Bank of England has cut interest rates six times since the current government took office, providing some relief to mortgage holders and businesses. But the divergence between Bank Rate and gilt yields — which are set by market forces rather than the Monetary Policy Committee — reflects investor concerns about inflation, geopolitical risk, and the long-term sustainability of UK public finances.

Key Developments

On Wednesday 6 May, thirty-year gilt yields reached 5.78% — a level not seen since the late 1990s. Ten-year yields exceeded 5%. The immediate trigger was a combination of factors: the ongoing disruption to Middle East oil supply routes caused by the US-Iran conflict, which has pushed Brent crude to approximately $107 per barrel; political uncertainty ahead of Thursday's local elections; and broader global investor nervousness about the trajectory of US fiscal policy under the Trump administration.

HSBC shares fell on Wednesday following a report of weaker-than-expected quarterly profits and an increase in expected credit losses totalling $1.3 billion. Barclays, NatWest, Lloyds, and Standard Chartered also declined. EY reported that loan growth at UK challenger banks had slowed sharply, from 8.9% to 4.5%, as customers prioritised debt repayment over new borrowing.

Global equity markets, by contrast, rallied on Wednesday on hopes that a US-Iran deal was close, with oil prices falling from recent highs. The FTSE 100 closed around 10,373, recovering some of the ground lost in recent sessions. Sterling traded at approximately 1.3594 against the US dollar.

Why It Matters

Rising gilt yields matter for every household in the UK. Higher government borrowing costs feed through into mortgage rates — particularly for those on tracker or variable-rate deals — and into the cost of business loans. For the government, each percentage point increase in gilt yields adds billions to the annual debt servicing bill, crowding out spending on public services. The Prime Minister has already warned that inflation could rise above 6% if oil prices remain elevated — a prospect that would represent a significant reversal of the progress made in bringing inflation down from its post-pandemic peak.

For context, the UK's debt-to-GDP ratio is already at levels not seen since the 1960s. Unlike Germany, which has maintained a constitutional debt brake, or the United States, which benefits from the dollar's reserve currency status, the UK has limited fiscal buffers. The combination of high debt, rising yields, and geopolitical uncertainty is a particularly uncomfortable one for a government that came to power promising economic stability.

Local Impact

In Northern Ireland, where the housing market has been more insulated from the worst of the mortgage rate rises than parts of England, the impact of rising gilt yields is nonetheless felt through public spending constraints. The Stormont Executive's block grant is determined by the Barnett formula, which is itself constrained by Westminster's fiscal position. In the Republic of Ireland, where the economy has been more resilient, the contrast with UK borrowing costs is stark — Irish ten-year bond yields remain significantly below UK equivalents, reflecting the different fiscal trajectories of the two economies.

What's Next

The Bank of England's Monetary Policy Committee meets in June, and markets will be watching closely for any signal that the pace of rate cuts will slow in response to inflationary pressures from oil prices. The Chancellor is expected to present an updated fiscal statement in the autumn, at which point the full impact of higher gilt yields on the public finances will be clearer. In the near term, Thursday's local election results will be the dominant political story — but the gilt market will be watching too.

Sources: CPA UK Business News, Financial Times