UK Housing Market Holds Steady in April But Rising Mortgage Rates Cast Shadow

The UK housing market is displaying cautious stability this spring, with supply at an eleven-year high and prices broadly flat, but rising mortgage rates driven by geopolitical instability are dampening buyer confidence and complicating the outlook for the months ahead.

Key Developments

The average UK house price stood at approximately £270,500 in February 2026, with Rightmove reporting a typical 0.8% spring rise in new seller asking prices in March to £371,042. However, annual asking price growth remained negative at -0.2%, reflecting the subdued market conditions that have persisted since the post-pandemic boom faded.

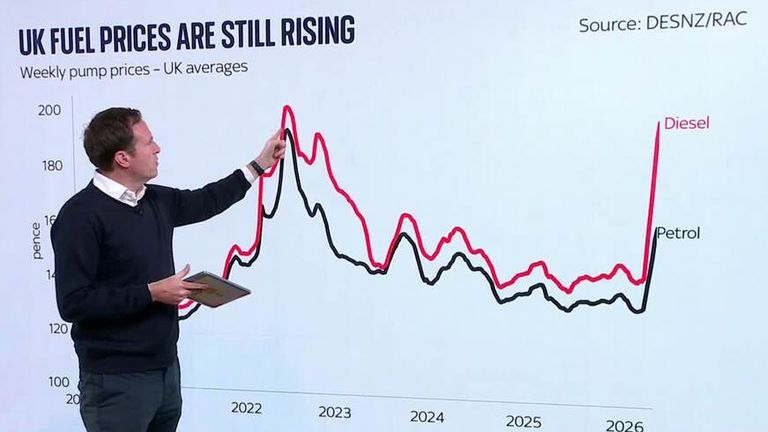

The Bank of England held its base rate at 3.75% at its March meeting and is widely expected to maintain this position at its April 30th decision, as UK inflation at 3% remains above the 2% target. This caution has been amplified by the conflict in the Middle East, which has disrupted global energy markets and pushed the average two-year fixed mortgage rate to 5.9% on April 8th — its highest level since July 2024.

Regional Divergence

The market is showing pronounced regional variation. Northern Ireland is the standout performer, with annual house price growth of 8.7% according to Halifax and 9.5% according to Nationwide — figures that reflect strong local demand and relatively affordable prices compared to the rest of the UK. By contrast, prices have fallen in London and the South East, where affordability pressures are most acute.

Background

The supply of homes for sale is at its highest level in eleven years, giving buyers significantly more choice than they have enjoyed for much of the past decade. This increased supply, combined with higher borrowing costs, has shifted the balance of power in negotiations towards buyers in many parts of the country.

Before the Middle East conflict escalated, markets had anticipated two base rate cuts in 2026. Many analysts now predict the rate will be held at 3.75% for the remainder of the year, with Oxford Economics forecasting that inflation will peak at 4% in the fourth quarter before falling back.

Why It Matters

For the millions of UK homeowners coming off fixed-rate deals in 2026, the prospect of higher mortgage costs represents a significant financial challenge. The housing market's performance is also closely watched as a barometer of broader consumer confidence and economic health.

What's Next

All eyes will be on the Bank of England's April 30th rate decision and any signals about the future path of interest rates. Estate agents advise sellers to price correctly from the outset, noting that around 340 properties in a typical mid-sized UK market reduced their asking price in March alone — the highest figure seen in some time. For buyers, the current conditions offer more time to make decisions and greater opportunity to negotiate.