UK Economy Stagnates as Middle East Conflict Upends Growth Forecasts and Rate Cut Hopes

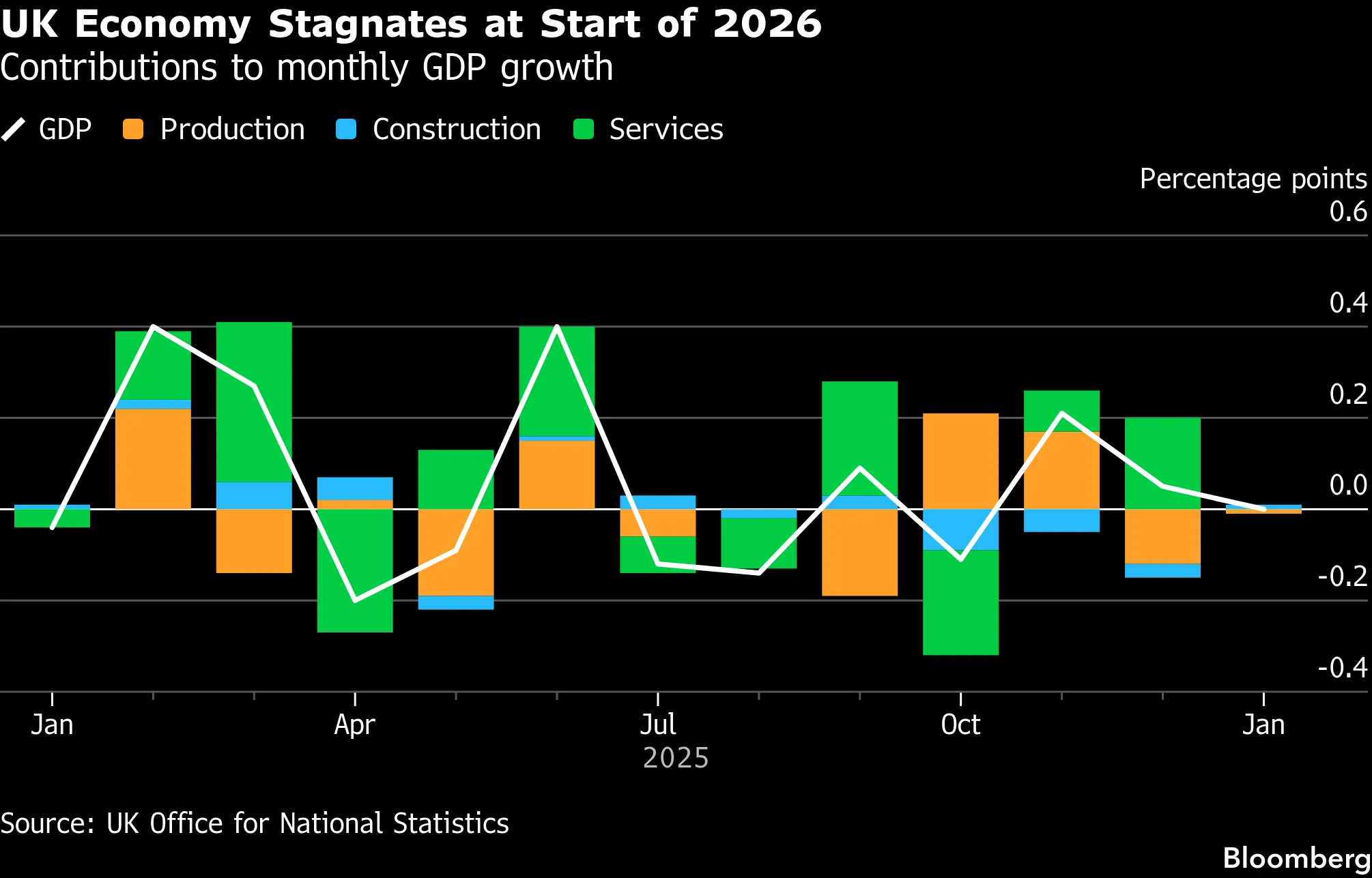

The British economy has ground to a halt, with new figures confirming near-zero growth and rising unemployment, as the escalating conflict in the Middle East throws optimistic forecasts into disarray and extinguishes hopes of imminent interest rate cuts. Data shows the UK's Gross Domestic Product (GDP) grew by a mere 0.1% in the final quarter of 2025 before flatlining completely in January 2026. Compounding the gloom, unemployment rose to 5.2% in the three months to January, painting a grim picture of a nation caught in a stagflationary trap of stagnant growth and persistent inflation.

Background

The current economic malaise follows a brief period where a recovery seemed to be taking hold. After a challenging 2024, the Bank of England had begun a cautious cycle of monetary easing, starting with a rate cut in August 2024, in an attempt to breathe life back into the economy. The initial signs were promising, with inflation beginning to cool and consumer confidence showing tentative signs of improvement. Forecasters had widely predicted a "soft landing," where inflation would return to its 2% target without triggering a major economic downturn. This narrative allowed the government to project a sense of returning stability after the turbulence of the post-pandemic years.

However, that narrative has been shattered by a combination of stubborn domestic weakness and a severe external shock. The underlying fragility of the UK economy was exposed by the latest GDP figures, which revealed that the country had effectively stopped growing at the turn of the year. The expected consumer-led recovery failed to materialise, as households continued to grapple with the high cost of living. Business investment also remained subdued, reflecting a deep-seated lack of confidence in the country's economic prospects.

This domestic weakness has been dangerously amplified by the geopolitical turmoil in the Middle East. The conflict involving Iran has sent energy prices soaring, directly feeding into UK inflation and undoing much of the progress made over the past year. The situation has forced a painful reassessment among economists and policymakers, with the prospect of rate cuts now receding into the distant future. The latest economic data from the House of Commons Library underscores the severity of the challenge, confirming the UK's position as a laggard among advanced economies.

Key Developments

The divergence in economic forecasts highlights the profound uncertainty gripping the market. Oxford Economics, a respected consultancy, has adopted a deeply pessimistic outlook, stating its belief that interest rates will now remain at their current level of 3.75% not only through the rest of 2026 but well into 2027. This represents a dramatic reversal from just a few months ago when multiple rate cuts were expected this year. In stark contrast, analysts at JP Morgan are predicting that the Bank of England will be forced to go further, forecasting a rate increase as early as June to combat the renewed inflationary threat from energy prices.

The National Institute of Economic and Social Research (NIESR) has warned of an even more severe scenario, suggesting that rates could climb as high as 4.5% if elevated energy costs become entrenched. This would have significant consequences for mortgage holders and businesses, likely pushing the fragile economy into a recession. Bank of England Governor Andrew Bailey, speaking after the latest rate decision, acknowledged the "highly uncertain" environment, offering little comfort to those hoping for a clear path forward. He stressed that the Monetary Policy Committee would remain data-dependent, responding to events as they unfold.

Alongside its interest rate policy, the Bank is also continuing its programme of quantitative tightening (QT). The Bank confirmed that it has reduced its total asset holdings from a peak of £895 billion to £529 billion by 11th March 2026. It plans to reduce this by a further £70 billion over the year to September 2026. As one Bloomberg analysis notes, this dual tightening of interest rates and QT presents a significant headwind for growth.

Why It Matters

The stagnation of the UK economy is a crisis that extends far beyond the realm of statistics and forecasts. It signals a potential long-term decline in British living standards and a fundamental challenge to the country's economic model. The dream of a swift recovery from the pandemic has evaporated, replaced by the grim reality of stagflation. This situation leaves the government with no easy options. Fiscal stimulus, such as tax cuts or increased spending, would risk pouring fuel on the inflationary fire. However, austerity measures would further depress demand and could trigger a deep recession. This economic paralysis has profound political implications. Public frustration with the cost of living, stagnant wages, and deteriorating public services is likely to intensify. The government's narrative of economic competence is becoming increasingly difficult to sustain. The crisis also raises difficult questions about the UK's resilience to external shocks. The economy's heavy reliance on imported energy has left it dangerously exposed to geopolitical events, highlighting a long-term failure to invest in energy security and alternative power sources.

Local Impact

For the average person in Britain, economic stagnation translates into a tangible decline in their quality of life. The 5.2% unemployment rate means that hundreds of thousands of people are now without a job, and many more will fear for their job security. For those in work, wage growth is unlikely to keep pace with the resurgent inflation, meaning a real-terms pay cut. This squeeze on disposable income will be felt across the country, as families are forced to cut back on non-essential spending. The dream of homeownership will recede for many, as high interest rates and economic uncertainty make mortgages less affordable. Local businesses, particularly in the retail and hospitality sectors, will be at the sharp end of this downturn. With consumers tightening their belts, many small and medium-sized enterprises will struggle to survive.

What's Next

The immediate future for the UK economy looks bleak. The next few months will be critical in determining whether the country can avoid a recession. The Bank of England will continue to monitor the data, but its options are limited. A rate hike in June remains a distinct possibility if inflation does not show signs of abating. The government, meanwhile, is under immense pressure to act. The upcoming Autumn Statement will be a crucial test of its ability to devise a credible plan for growth without exacerbating inflation. Much will depend on events beyond the UK's borders. A resolution to the conflict in the Middle East would provide immediate relief, but this is far from certain.