Tesla Beats Q1 2026 Earnings Estimates with $22.4B Revenue and 21.7% Gross Margin

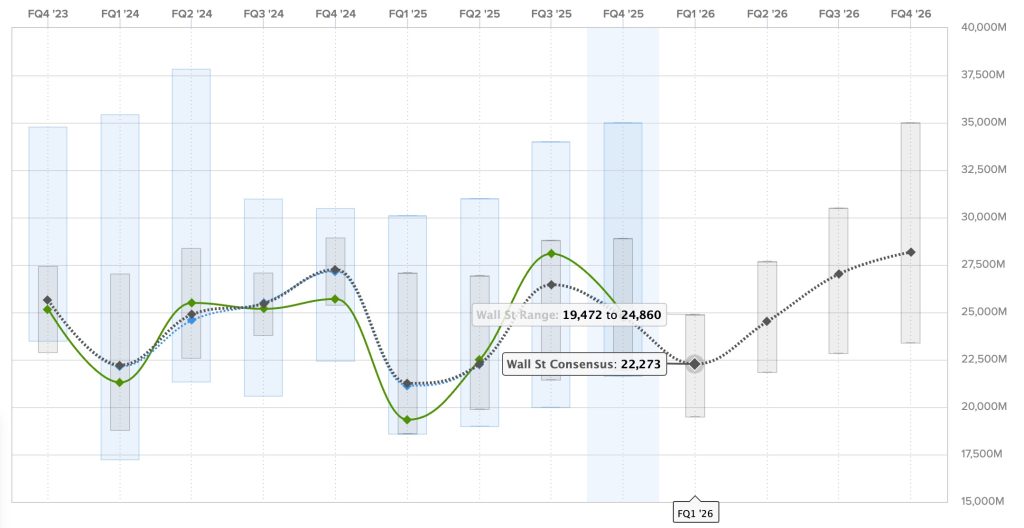

Tesla delivered a stronger-than-expected first quarter on April 22, 2026, reporting revenue of $22.39 billion and adjusted earnings per share of $0.41 -- both ahead of analyst forecasts -- while posting a gross margin of 21.7% that significantly outpaced the consensus estimate of 17.7%. The results provided a much-needed boost to investor confidence in the electric vehicle maker after a turbulent start to the year.

Background

Tesla entered 2026 under considerable pressure, with vehicle deliveries in the first quarter coming in at 358,023 units -- below some prior forecasts -- amid intensifying competition from Chinese EV manufacturers and softening demand in key markets. Chief Executive Elon Musk's high-profile political activities had also drawn scrutiny from some investors and consumers, contributing to brand perception challenges in certain markets. Against this backdrop, the earnings beat was seen as a significant positive signal.

Key Developments

The company's Q1 revenue of $22.39 billion exceeded the analyst consensus estimate of $22.08 billion, while adjusted EPS of $0.41 beat the $0.35 estimate by a meaningful margin. The standout figure was the gross margin of 21.7%, which came in well above the 17.7% estimate, suggesting that Tesla's cost reduction efforts and manufacturing efficiencies are bearing fruit despite lower delivery volumes.

On the earnings call, Tesla executives highlighted progress on the company's robotaxi programme and its Optimus humanoid robot initiative as key drivers of future growth. Management expressed confidence that the robotaxi service, which has been undergoing testing in select US cities, would begin generating meaningful revenue in the second half of 2026. The Optimus robot, intended for both industrial and consumer applications, was described as on track for limited commercial deployment by year-end.

Why It Matters

The earnings beat is significant for several reasons. It demonstrates that Tesla's core automotive business remains profitable even as the company invests heavily in next-generation technologies. The gross margin improvement, in particular, suggests that the company has successfully navigated some of the cost pressures that weighed on results in 2025. For the broader EV sector, Tesla's performance provides a data point that premium electric vehicles can maintain strong margins even in a more competitive market environment.

The results also come at a critical juncture for Tesla's stock, which had underperformed the broader market in early 2026. The after-hours rally following the earnings release helped recover some of that lost ground and may signal renewed institutional interest in the company's long-term growth story.

What's Next

Investors will be watching closely for updates on the robotaxi launch timeline and any guidance on Q2 delivery targets. Analysts will also scrutinise whether the gross margin improvement is sustainable as Tesla navigates ongoing pricing pressures in the global EV market. The company's next major product event is expected in the summer, where new details on the Optimus robot and the next-generation affordable vehicle platform are anticipated.

Sources: Electrek; The Motley Fool; CNBC